What it means for estate planning and your family.

When planning a will, many people want to ensure a loved one can continue living in the family home after they pass away. While this can provide security and peace of mind, recent guidance from the Australian Taxation Office (ATO) highlights that the way this right is documented can have important capital gains tax (CGT) consequences.

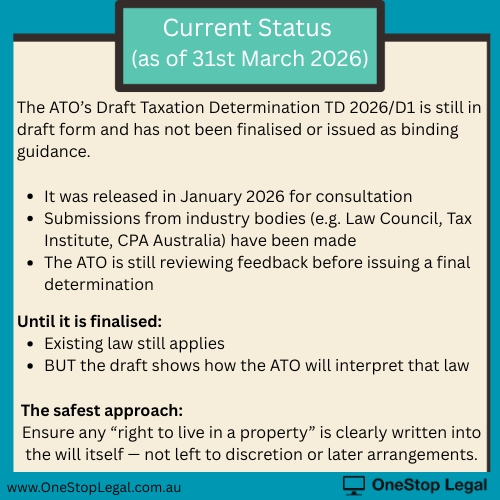

The ATO has released a draft ruling (TD 2026/D1) which clarifies when a property may still qualify for CGT exemptions if someone has the right to live in it after the owner’s death.

At OneStop Legal, we’re seeing this issue come up more often in estate planning — particularly where wills include rights of residence or life interests.

Why This Draft Ruling Matters

Under current tax law, a capital gain on a deceased person’s home may be disregarded if:

- the property is sold within certain timeframes, or

- It is occupied as a main residence by a person who has a right to live in the property under the will.

The ATO’s draft ruling makes it clear that not all living arrangements qualify. Only very specific rights will preserve the CGT exemption.

What the ATO Says Counts as a “Right to Live in the Property”

According to the draft ruling, a qualifying right must:

- be clearly and expressly written into the will (or a valid codicil)

- identify who has the right to live in the property

- apply automatically under the will, without needing later decisions or agreements

If these elements are missing, the CGT exemption may not apply when the property is sold.

What Does Not Qualify

The ATO has confirmed that the following arrangements generally do not qualify as a right to live in the property for CGT purposes:

- where the executor or trustee simply has discretion to let someone live there

- informal family arrangements or side agreements

- rights created only under a testamentary trust deed

- occupancy granted after death without being stated in the will

Even if everyone agrees on the arrangement, the tax outcome may be different if it is not properly documented.

Why This Can Affect Capital Gains Tax

If a right to live in the property does not qualify:

- the CGT main residence exemption may be reduced or lost

- the estate or beneficiaries may face unexpected tax when the property is sold

- the CGT “cost base reset” may not operate as expected

This can significantly impact the value passed on to beneficiaries.

What This Means for Estate Planning

The key takeaway is simple:

If you intend for someone to live in a property after your death and want to preserve CGT concessions the right must be clearly drafted into your will.

This is especially important for blended families, second marriages, and estates where property is intended to pass to children after a surviving partner’s lifetime.

How OneStop Legal Can Help

At OneStop Legal, we assist clients with:

- drafting and updating wills

- reviewing estate plans involving property and life interests

- working alongside accountants and advisers to minimise tax risks

- providing clear, practical advice for executors and beneficiaries

If your will includes property or you’re unsure how your estate plan may be treated for tax purposes it’s worth getting advice before problems arise. Contact us today to see how we can help!